Auto loans shape more than your monthly payment, they influence your long-term financial flexibility and total cost of ownership. With the right preparation, you can make confident financing decisions that support your budget.

Buying a car is one of the few financial decisions that affects your daily life. It gets you to work, helps you take care of responsibilities, and gives you flexibility when plans change. What’s often overlooked is that the financing matters just as much as the vehicle itself.

The good news is that saving money on a car loan doesn’t require complex strategies. A few informed choices, especially before you visit a dealership, can make your next car significantly more affordable over time.

Let’s break down how auto loans work, what affects your rate, and how everyday financial habits can help you save, without the pressure or sales talk.

Why Auto Loan Decisions Matter More Than You Think

When most people shop for a car, they focus on the sticker price or monthly payment. Both matter, but they don’t tell the full story. How your loan is structured plays a major role in your overall financial picture.

Your interest rate, loan term, and loan setup directly affect:

- Your total cost over time, by determining how much interest accrues

- Your monthly breathing room, by shaping how manageable payments feel

- Your future flexibility, including the ability to refinance or pay ahead

Understanding these elements upfront helps you make decisions based on long‑term stability, not just up-front affordability.

Why Pre‑Approval Can Change the Car Buying Experience

Getting pre‑approved for an auto loan before shopping is one of the best ways to reduce uncertainty.

Pre‑approval gives you clarity before you ever step onto the lot. It allows you to:

- Know your realistic budget based on an approved loan amount

- Compare vehicles confidently within your financing range

- Avoid rushed, high pressure financing decisions at the dealership

- Focus on total loan cost, not just the monthly payment offered

Many credit unions, including First Entertainment, let you explore financing without committing to a purchase. This approach reflects relationship-based lending that prioritizes education, transparency, and affordability over speed alone.

How Your Financial Habits May Affect Your Auto Loan Rate

While your credit score is important, it’s not the only factor lenders may consider. Some also look at how you manage your money day by day.

For example, they may look for:

- Verified income through direct deposits

- Automatic payments on new or existing loans

- A loan amount that aligns closely with the vehicle’s value

These behaviors can lower risk for lenders and, in some cases, support more favorable loan terms. Since underwriting criteria vary, understanding which habits matter, and whether changes fit your broader financial goals, puts you in a stronger position.

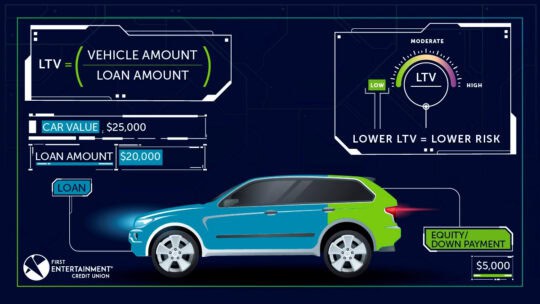

Loan-to-Value (LTV): A Simple Metric with Big Impact

Loan‑to‑value (LTV) compares how much you’re borrowing to how much the car is worth. Borrowing closer to the vehicle’s value generally makes a loan less risky from a lender’s perspective.

LTV is influenced by the vehicle price and your down payment. Keeping your loan amount in balance with the car’s value can lead to better terms and greater flexibility later, whether you plan to refinance, sell the car, or adjust your budget.

Choosing the Right Loan Term for Your Situation

Auto loans come in a range of terms, and each option involves tradeoffs.

Shorter terms usually mean higher monthly payments, but less interest paid overall. Longer terms tend to lower monthly payments while increasing total interest costs. The right choice depends on your cash flow, financial priorities, and how long you plan to keep the vehicle. A supportive lender will walk through different scenarios with you, helping you understand how each option fits your lifestyle and budget.

Whether you’re shopping now or planning ahead, understanding auto loans puts you in control early and helps your next car support your financial well-being, not just your commute.